On Jan. 16, 2019, Agilent Technologies announced the addition of SAP executive Mala Anand to its Board of Directors. Agilent is a well regarded company with a $23 billion market cap on annual revenue of $4.9 billion. When new members join a company’s board, Watchdog Reports will often review the company to asses the company’s quality of financial disclosures.

Watchdog’s Concerns

The Agilent Corporate Watchdog Report (attached) provides information about a company’s audit committee, outside auditor, CFO and SEC interest. In the case of Agilent, we found some concerns.

Before we delve into our concerns, let’s establish the complexity and accounting challenges Agilent is likely grappling with and give a quick review of Agilent’s history of accounting accuracy.

First, we note that Agilent operates three lines of business. Accounting for three lines is far more complicated than one line. Likewise, we note that Agilent operates across many countries, each with various tax and financial disclosure laws. Finally, we note that Agilent has grown via acquisitions. It has made 46 in the past 18 years and a surprising six in the last year. Accounting for acquisitions is a very complicated task.

Against this backdrop of significant operating complexity, we note that Agilent has also made at least seven different financial restatements and out-of-period adjustments in the last ten years and has had at least one 404 and one 302 adverse disclosure about weak controls. All these speak to weakness in Agilent’s accounting disclosures.

Given this assessment, we would expect to see significant investments by Agilent in resources and people behind its financial disclosures. Let’s work our way up through the various layers of those resources to evaluate what we found.

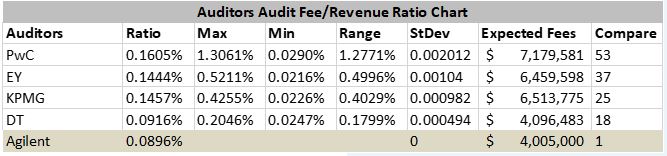

We start with the CFO. Less than five months ago, Agilent hired a new, outside CFO. A new CFO requires time to learn the business. Fortunately, the company has had PWC as its auditor for 20 years. But we found troubling issues with PWC. Namely, PWC was paid 33% LESS in 2018 than the firm was paid on average for the last 10 years. Paying an auditor less means less auditing.

How much auditing is enough? We took a look at audit fees for similar-sized PWC clients and peers of Agilent to estimate an estimated auditor fee. Take a look at the table at the bottom. You’ll see our analysis suggests the company should be paying PWC roughly $7million. That is 73% more than the $4 million the company paid last year. Cutting down on audit fees seems unwise for Agilent.

How about Agilent’s Audit Committee? Well, its Audit Chair is Paul N. Clark. His bio is heavy on industry knowledge and strategic planning, but weak on deep financial or audit experience. We looked over Agilent’s other Audit Committee members and could not find any member with extensive financial disclosure or audit experience. We don’t like that.

After its CFO, auditors and audit committee members, the last line of defense an investor should consider is the SEC. Here we found weak SEC interest in Agilent. The last SEC correspondence was in 2016 and was related to the company doing business in Syria.

Bottom line: Agilent’s financial disclosure and reporting history is weak. It now has a new CFO, seems to be under investing in its audit and has growing complexity in its business. We would like to see more rigor in Agilent’s disclosures and we hope the new board member demands that.